Updated January 2025

The Inflation Reduction Act (IRA) has changed the face of many industries since  becoming law on August 16th, 2022. The automotive industry is no exception, as a wide range of IRA measures seek to revitalize domestic supply chains and accelerate the transition to electric vehicles. That impact continues to play out, and a variety of post-dated measures and recent modifications are changing how the industry handles supply chain traceability and material sourcing.

becoming law on August 16th, 2022. The automotive industry is no exception, as a wide range of IRA measures seek to revitalize domestic supply chains and accelerate the transition to electric vehicles. That impact continues to play out, and a variety of post-dated measures and recent modifications are changing how the industry handles supply chain traceability and material sourcing.

From original equipment manufacturers (OEMs) to Tier 1, 2, and 3 automotive suppliers, every organization across the automotive supply chain has had to adapt to these changes, and will have to continue doing so into the future. Read on to see how the IRA has affected the industry so far, the most recent changes for 2025, and what to expect on the horizon.

Table of Contents

Inflation Reduction Act of 2022 Summary

Inflation Reduction Act 2023 Changes

Prohibitions on Foreign Entities of Concern

2025 Material Sourcing Requirement Updates

The Impact of the IRA on the US Automotive Industry

How OEMs Demonstrate Eligibility for Inflation Reduction Act Benefits

How Auto Suppliers Can Provide OEMs With the Data They Need

Taking Action on Supply Chain Sourcing and Traceability

Inflation Reduction Act of 2022 Summary

The Inflation Reduction Act contains a variety of tax credits and other measures designed to encourage the sale of electric vehicles (EVs) and the use of domestic parts and materials throughout the automotive industry. Many of these changes focused on section 30D of the Internal Revenue Code. This section dates back to the Energy Improvement and Extension Act of 2008, when it established a new clean vehicle tax credit of up to $7,500 for the purchase of plug-in EVs, and has undergone a variety of changes since.

The majority of the changes enacted by the IRA concerning section 30D will come into effect at later dates. However, one of the most significant changes took effect on day one. The IRA modified section 30D such that only vehicles that undergo final assembly in North America are eligible for the tax credit.

The majority of the changes enacted by the IRA concerning section 30D will come into effect at later dates. However, one of the most significant changes took effect on day one. The IRA modified section 30D such that only vehicles that undergo final assembly in North America are eligible for the tax credit.

This and later measures aimed to put additional pressure on OEMs to bring their supply chains back to the US and North America in general. Having their EVs eligible for the credit provides a clear market advantage for OEMs. With the implementation of the IRA, OEMs faced a variety of new conditions if they wanted to keep it that way.

Inflation Reduction Act 2023 Changes

As the IRA became law just over halfway through 2022, many of its measures took effect on January 1st, 2023. That includes several additional changes to section 30D.

First, the IRA repealed the existing production cap on the new clean vehicle tax credit. Before the IRA, the tax credit included a limit of 200,000 EVs per OEM. Once past that limit, additional units were not eligible for the tax credit. At the time of the IRA passing, both Tesla and GM had already reached the cap, meaning their vehicles were no longer eligible. Toyota and other OEMs were rapidly approaching it as well. As of January 1st, 2023, this restriction no longer applies, making Tesla and GM EVs eligible again.

Another part of the amendment to section 30D was pending review by the US Treasury and the Internal Revenue Service (IRS), only coming into effect on April 18th, 2023. This amendment established the critical minerals and battery component sourcing requirements for the federal EV tax credit, one of the most significant changes for OEMs and auto suppliers.

The original $7,500 tax credit now consists of two distinct tax credits of $3,750 each, with vehicle models potentially qualifying for both, one, or neither. The EV batteries must meet specific sourcing requirements for critical minerals to be eligible for one tax credit and battery components for the other.

EV batteries must have 40 percent of the critical minerals contained within them sourced from the US or its free trade partners to remain eligible for the tax credit. For battery components, 50 percent must be manufactured or assembled in North America. However, these are only the initial values for 2023. The IRA also established a series of scheduled increases for both criteria.

Another change to the federal tax credit for electric cars 2023 brought with it is the inclusion of commercial vehicles. The IRA added section 45W to the Internal Revenue Code, establishing tax credits for commercial vehicles. Tax credits are available for up to 30 percent of the vehicle value, up to $7,500 for vehicles under 14,000 lbs and $40,000 for vehicles above 14,000 lbs.

This tax credit is only available up to 15 percent of the vehicle value if the vehicle is gas or diesel-powered (i.e., hybrid electric vehicles). The critical mineral and battery component requirements that affect consumer vehicles do not apply to commercial vehicles.

Organizations across the supply chain are seeking out solutions to meet new sourcing requirements. OEMs and auto suppliers already achieve excellent return on investment with the right EMS to handle other EHS needs, and they now have to hope their current providers can meet their needs or look elsewhere.

While these new requirements pose supply chain traceability and sourcing challenges for OEMs and automotive suppliers, the shift toward domestic production introduced new opportunities for manufacturers at every level of the supply chain.

The Advanced Manufacturing Production Credit

The Advanced Manufacturing Production Credit (section 45X) is another major component of the IRA’s amendments to the Internal Revenue Code. It established a wide range of clean and renewable energy tax credits, covering everything from solar and window power to carbon capture and smart grid technology. The program also includes substantial tax credits for the production of EV batteries.

Section 45X establishes four distinct tax incentives for domestic EV battery production, allowing manufacturers to claim up to:

- 10 percent of the cost of critical mineral production

- 10 percent of the cost of electrode active material production

- $35 per kWh of battery cell production

- $10 per kWh of battery module assembly

To qualify for these tax incentives, manufacturers must carry out the specific production or assembly activity within the United States. Looking at production and assembly credits for 2023’s top-selling US electric vehicles alone, it is clear that the Advanced Manufacturing Production Credit will be a major incentive to move EV battery supply chains stateside.

|

Vehicle |

Battery Capacity (kWh) |

Maximum Tax Credit (USD) |

|

|

Cell Production |

Module Assembly |

||

|

Tesla Model Y |

80.5 |

2817.50 |

805.00 |

|

Tesla Model 3 |

80.5 |

2817.50 |

805.00 |

|

Chevrolet Bolt |

63 |

2205.00 |

630.00 |

|

Ford Mustang Mach-E |

88 |

3080.00 |

880.00 |

|

Volkswagen ID.4 |

77 |

2695.00 |

770.00 |

|

Hyundai Ioniq 5 |

77.4 |

2709.00 |

774.00 |

|

Rivian R1S |

128.9 |

4511.50 |

1289.00 |

|

Ford F-150 Lightning |

131.0 |

4585.00 |

1310.00 |

|

Tesla Model X |

100.0 |

3500.00 |

1000.00 |

|

BMW i4 |

81.5 |

2852.50 |

815.00 |

After a public hearing in February 2024, the IRS published the final rule laying out specific rates and criteria for these tax incentives in October 2024.

Prohibitions on Foreign Entities of Concern

As of 2024, additional restrictions and increased various requirements for the new clean vehicle tax credit came into effect. The industry faces stricter critical mineral and battery component thresholds, along with the introduction of Foreign Entity of Concern (FEOC) restrictions. EVs with batteries or battery components manufactured or assembled by FEOCs are not eligible for tax credits.

Missing out on the new clean vehicle tax credit isn’t the only cause for concern for companies working with FEOCs. The Bipartisan Infrastructure Law (BIL), signed into law in 2021, established $3.5 billion in battery materials processing and manufacturing grants to support and strengthen domestic supply chains. Organizations with FEOCs in their supply chains are ineligible for these grants.

These changes have made supply chain traceability more critical for the automotive industry than ever before. OEMs know that their EVs are much more competitive when they are eligible for the new clean vehicle tax credit, and they choose their suppliers accordingly. With a wide range of incentives and funding on the line, EV battery supply chains can’t afford to mix with FEOCs.

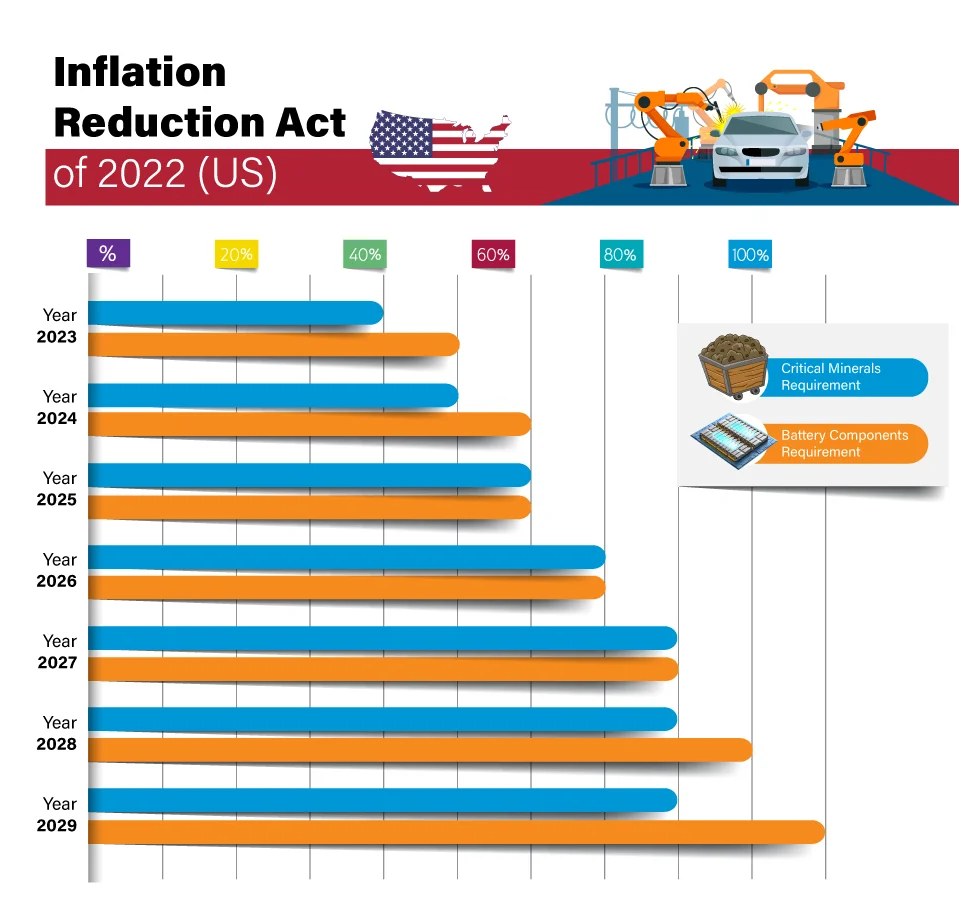

2025 Material Sourcing Requirement Updates

The coming years will increase restrictions on automotive suppliers and OEMs. Many of the requirements put in place by the IRA feature scheduled increases on a year-by-year basis. The relationship between OEMs and auto suppliers means that this will continue to exert pressure on suppliers to improve traceability and sourcing.

As of 2025, FEOC restrictions now extend to cover critical minerals as well. While 2024 changes only affected battery component manufacturing and assembly, vehicles with batteries containing critical minerals extracted, processed, or recycled by FEOCs are now ineligible for the new clean vehicle tax credit.

The existing requirements for critical mineral sourcing from the US or free trade agreement partners and battery component sourcing from North America will become stricter in the future. Over the coming years, the IRA will gradually increase the critical minerals sourcing requirement to 80 percent in 2027 and the battery components sourcing requirement to 100 percent in 2029.

The Impact of the IRA on the US Automotive Industry

The IRA has implemented a wide range of tax incentives, direct investment, and other measures to push the US automotive industry toward EV adoption and stronger domestic supply chains. The results over the course of 2022 and 2023 show success in both areas.

While the market is too complex to deem IRA tax incentives as the sole cause of growth, EV sales have increased significantly. EVs accounted for 9.1 percent of passenger vehicle sales in 2023, up from 6.8 percent in 2022. Total US EV sales in 2023 reached 1.4 million, a 50 percent increase from 2022.

The US Energy Information Administration forecasts EV sales to account for up to 15 percent of light-duty vehicle sales by 2030 and up to 29 percent by 2050. This outlook arises from current trends and the unprecedented investment in domestic EV production that the IRA has spurred.

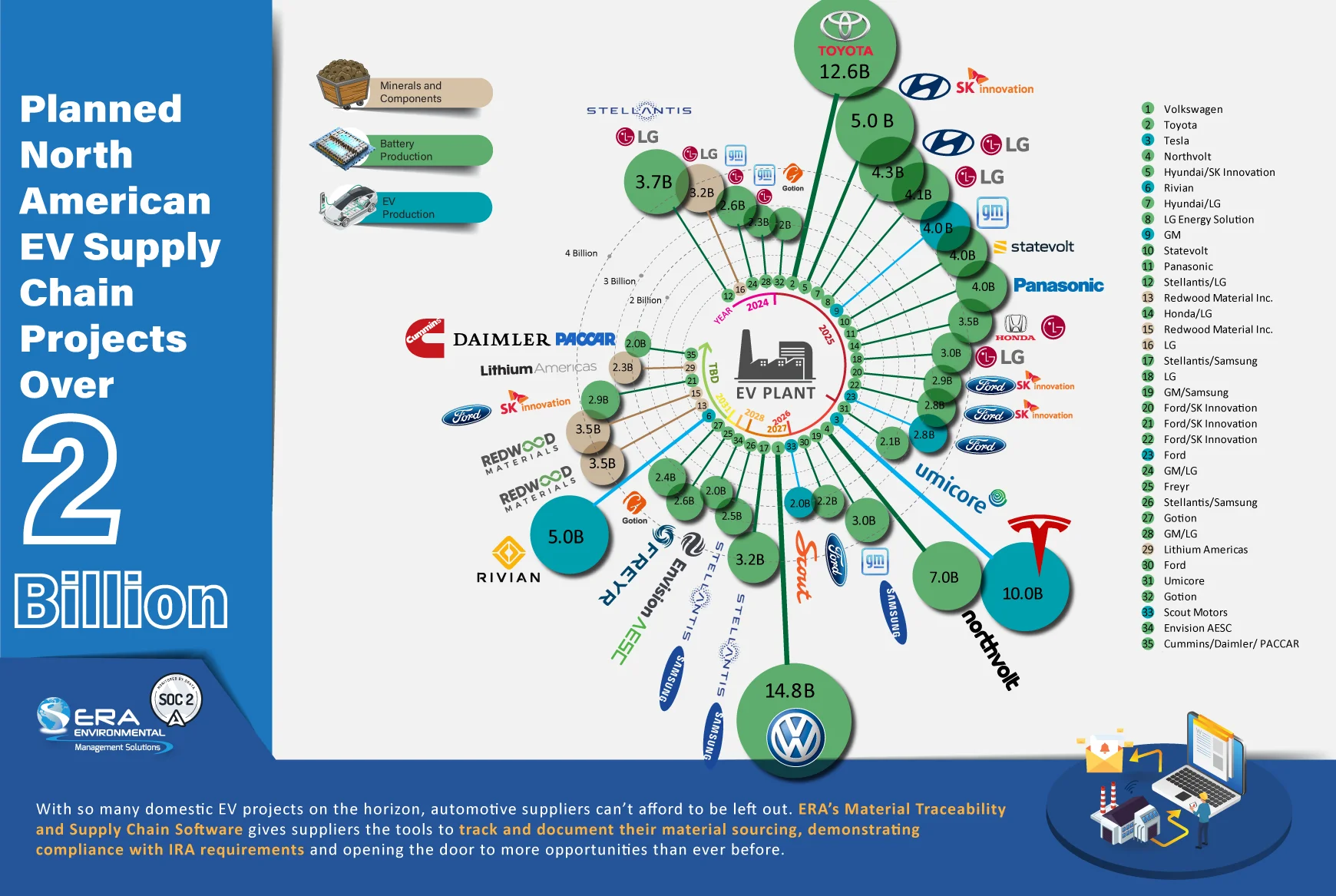

Planned Investments in Domestic EV Battery Manufacturing

Domestic electric vehicle and battery production will ramp up considerably over the coming years as many planned facilities begin their operations. Data from the US Department of Energy highlights over $167 billion in planned EV and battery production facilities on the horizon. Additional major projects within Canada and Mexico raise that total even higher.

This rapid development presents a unique opportunity for automotive suppliers to enter into lucrative long-term agreements as new supply chains form. OEMs need suppliers that produce materials and components within the United States and its free-trade partners to continue qualifying for incentives and investments as production ramps up.

How OEMs Demonstrate Eligibility for Inflation Reduction Act Benefits

The IRA sets out a variety of restrictions that OEMs must follow if their EV models are to be eligible for the new clean vehicle tax credit. To demonstrate compliance, OEMs must carry out a detailed accounting of materials and components across their supply chains and meet the specific standards established by the IRA.

Critical Minerals Traceability

Critical mineral procurement chains include the extraction and processing of new materials along with recycling and the processing of recycled materials. OEMs and battery manufacturers may have several suppliers for a given critical mineral, so each facility will likely have multiple procurement chains for each individual mineral.

OEMs and battery manufacturers must evaluate the procurement chain for each critical mineral in the battery, determining if extraction or processing took place in the US or in any free trader partner, or if recycling took place in North America. As of 2025, this also includes verifying that the procurement chain is free of any FEOCs.

The evaluation for critical minerals focuses on the value added across procurement chain steps. Qualifying materials have 50 percent or more of their added value originating from extraction or processing in the US or its free trade partners, or from recycling in North America.

Having determined which of their critical minerals are qualifying materials, OEMs then sum that value and divide it by the total value of critical minerals in the battery. They then compare that value to the required threshold for that year, which is 60 percent in the case of 2025.

Battery Components Traceability

OEMs must determine what percentage of battery components within a battery were manufactured or assembled in North America. That means components where substantially all of the manufacturing or assembly activities for that component occur in North America, while individual parts that make up a component may originate elsewhere. OEMs must also verify that components do not originate from FEOCs.

Each battery component’s incremental value contributes to the components’ total value. This method requires finding the sum of the value of basic component materials (e.g., anode, cathode, electrolyte, separator) and then adding the incremental value added by each step during assembly into cells and modules.

The OEM then divides the value of all components manufactured or assembled in North America by the total value of all components in the battery. They then compare this result against the threshold value for that year, which is 60 percent in 2025.

How Auto Suppliers Can Provide OEMs With the Data They Need

OEMs must prove that the critical minerals and battery component sourcing for their electric vehicle batteries meet the above requirements if their models are to be eligible for new clean vehicle tax credits. Putting that into practice requires supply chain traceability and transparency from their suppliers. This shifts the pressure onto Tier 1, 2, and 3 suppliers to provide accurate and accessible supply chain data.

ERA’s Material Traceability and Supply Chain Software is a comprehensive solution that lets auto suppliers thrive in a landscape defined by increasing traceability requirements.

Collect all required documentation from upstream suppliers to trace the origin and processing locations of raw materials and value-added steps. ERA’s platform lets suppliers across the supply chain share this essential data, and it features custom material identification forms, allowing flexibility in your unique operations. Track sources and compositions and cross-reference with FEOCs.

Hold your raw material suppliers to the same stringent standards that your downstream supply chain expects. Built-in material sourcing assurance, physical location display, and e-signature verification ensure that your raw materials originate where your suppliers say they do and don’t co-mingle with other sources.

ERA’s software streamlines how you provide traceability data to OEMs and downstream supply chain partners with automated report generation. Deliver the key details needed to demonstrate new clean vehicle tax credit eligibility and compliance with other regulations, such as the Uyghur Forced Labor Prevention Act (UFLPA).

As critical mineral and battery component requirements only become stricter over the coming years, OEMs will have less flexibility in the suppliers they choose. Let ERA’s software ensure that your organization can check all of the boxes regarding supply chain sourcing and traceability.

Taking Action on Supply Chain Sourcing and Traceability

The Inflation Reduction Act has already changed the automotive industry landscape in the few short years that it has been in effect. The scheduled increases in supply chain sourcing and traceability requirements will continue to push OEMs to seek out additional domestic suppliers, opening the door to opportunities for those that can successfully demonstrate their compliance. The boom is already happening, with over $167 billion in new plants on the way. The time for suppliers to ensure that their supply chain sourcing and traceability are up to par is now.

There’s no reason why those suppliers have to navigate this transition alone. ERA’s Material Traceability and Supply Chain Software can automate and standardize workflows, eliminate manual data entry and management, and help suppliers provide the accurate and complete data OEMs look for. Schedule a discovery call with one of our project analysts today for more on what ERA can do for you.

References

Section 30D New Clean Vehicle Credit

Interpretation of Foreign Entity of Concern

Section 45X Advanced Manufacturing Production Credit

BIL 40207(b) Battery Materials Processing and 40207(c) Battery Manufacturing Grants

Clean Vehicle Tax Credits in the Inflation Reduction Act of 2022

Light Duty Electric Drive Vehicles Monthly Sales Updates

Building America’s Clean Energy Future

Contributing Scientist of This Article:

Comments